© Export Finance Australia

The views expressed in World Risk Developments represent those of Export Finance Australia at the time of publication and are subject to change. They do not represent the views of the Australian Government. The information in this report is published for general information only and does not comprise advice or a recommendation of any kind. While Export Finance Australia endeavours to ensure this information is accurate and current at the time of publication, Export Finance Australia makes no representation or warranty as to its reliability, accuracy or completeness. To the maximum extent permitted by law, Export Finance Australia will not be liable to you or any other person for any loss or damage suffered or incurred by any person arising from any act, or failure to act, on the basis of any information or opinions contained in this report.

GCC—Underlying resilience cushions conflict impacts

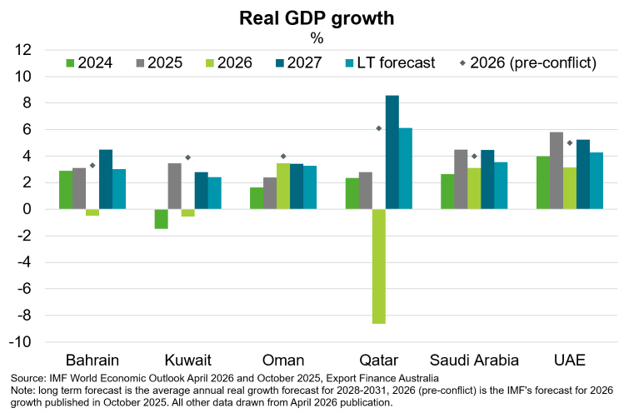

The Iran conflict is the most consequential shock to affect Gulf Cooperation Council (GCC) countries in recent history. GCC countries are experiencing disrupted energy and non-energy trade, physical damage to economic and civilian infrastructure, and damage to their reputations for safety and security in a challenging region. The IMF’s 2026 baseline growth forecast for the GCC overall was downgraded to 2% in April (from 4.3% in previous October forecasts), assuming that exports normalise by mid-year. While all forecasts were downgraded (Chart), only some will enter recessions. Qatar is most impacted following damage to its Ras Laffan LNG facilities, which provided about a fifth of the world’s LNG supply and will take years to fully recover. Oman, Saudi Arabia and the UAE are expected to have the strongest growth in the region, at 3.5%, 3.1% and 3.1% respectively. Economic damage would worsen if the conflict prolongs.

Most GCC countries entered the crisis with strong buffers that limit macroeconomic vulnerability, including low public debt, current account surpluses and well capitalised financial systems. Indeed, GCC sovereign wealth funds collectively managed around US$5.5 trillion in sovereign assets in Q1 2026. Growth downgrades are moderated due to ongoing operation of alternative port facilities—including Yanbu in Saudi Arabia and Fujairah in the UAE—and rapid adaptation of integrated logistics to increase throughput at Omani ports that bypass the Strait of Hormuz.

A durable peace agreement that re-opens the Strait of Hormuz would ease the logistical chokepoint. However, according to Wood Mackenzie, it would take three months for the region’s shut-in oil production to recover to 70% of pre-conflict levels, and up to six months to reach 90%. If the conflict intensifies or expands, longer term economic scarring becomes more likely, including through deferred investment, ongoing high import and transport costs, risk of further damage to infrastructure (including vulnerable water supplies), and structural supply chain shifts to reduce dependence on goods transiting the Strait of Hormuz. This would stifle new opportunities for Australian exports to the GCC, which nearly doubled over the five years to 2025, to over $12 billion.